OpEx vs CapEx: Definitions, Accounting, and Key Differences

Learn to classify OpEx vs CapEx correctly, understand the tax and accounting differences, and apply these rules to make smarter financial decisions.

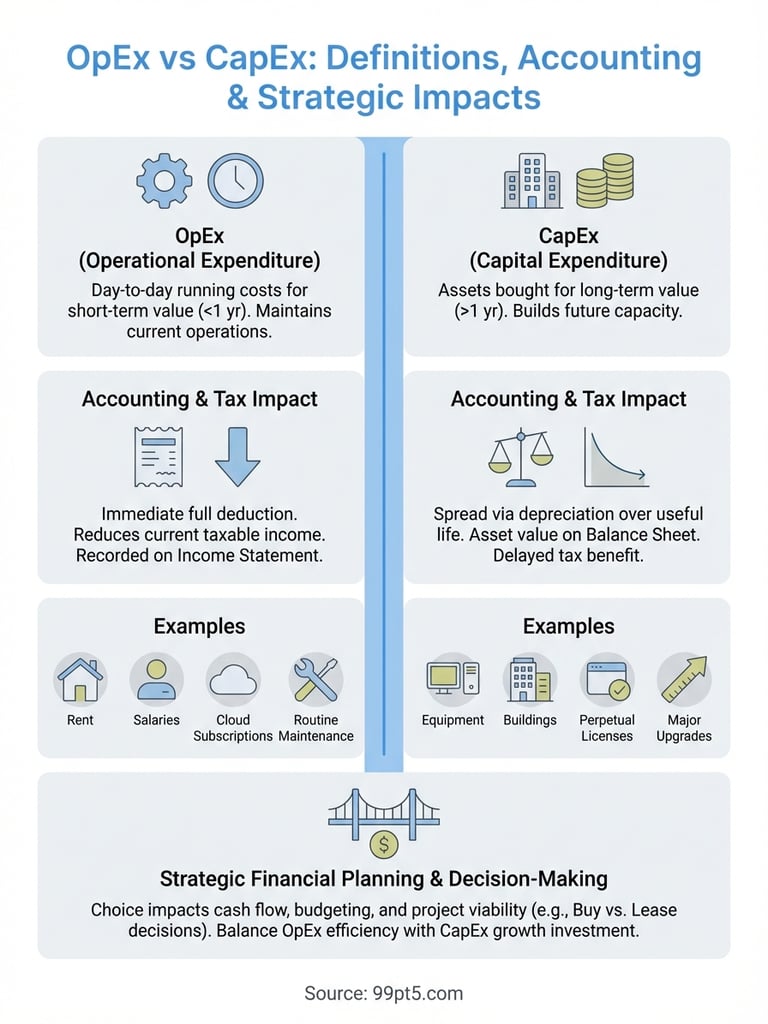

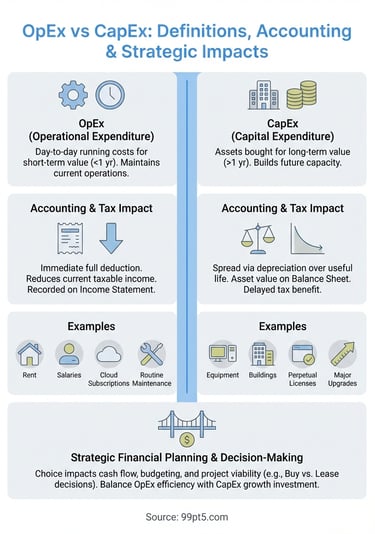

Every business decision about spending money comes down to one fundamental question: is this OpEx or CapEx? Operational expenditure covers your day to day running costs like salaries and utilities. Capital expenditure involves buying assets you'll use for years like equipment or buildings. The distinction affects how you record expenses, when you claim tax relief, and ultimately how much cash you keep in the bank.

This guide walks you through OpEx vs CapEx definitions, shows you how to classify expenses correctly in your accounts, and explains the accounting and tax treatment for each category. You'll see real examples from different industries, learn where the gray areas exist, and discover how to apply these concepts when evaluating capital projects. Whether you're assessing a new equipment purchase or reviewing your operating budget, understanding this difference helps you make smarter financial decisions and optimize your company's cash flow.

Why OpEx vs CapEx matters for your business

The way you classify spending between OpEx and CapEx directly impacts your cash flow planning, tax position, and financial reporting. When you record an expense as OpEx, you deduct the full amount in the current tax year, which reduces your taxable income immediately. CapEx spreads the cost across multiple years through depreciation, delaying your tax benefit but building asset value on your balance sheet.

Financial planning and decision-making

Your classification choice affects how you budget for major purchases and evaluate project viability. A piece of equipment classified as CapEx requires upfront capital approval and impacts your balance sheet, while an operating lease for the same equipment flows through as OpEx with lower initial investment. This distinction matters when you're choosing between buying equipment outright versus leasing it, or when you're deciding whether to upgrade infrastructure now or maintain existing systems.

Understanding OpEx vs CapEx helps you optimize your tax strategy and maintain healthy cash reserves for growth.

Banks and investors scrutinize both categories differently. High CapEx signals growth investment but ties up capital, while high OpEx relative to revenue can indicate operational inefficiency. You need to balance both to demonstrate financial health and operational discipline to stakeholders.

How to define OpEx and CapEx in your accounts

You classify expenses based on useful life and benefit duration rather than dollar amount alone. The fundamental test asks whether the expenditure creates value beyond the current accounting period. If you purchase something that helps your business for more than 12 months, you typically record it as CapEx. When the benefit expires within the current year, you classify it as OpEx.

Core criteria for OpEx classification

Operating expenses cover costs that maintain your current business operations without adding new capacity or extending asset life. You record rent payments, employee salaries, utility bills, software subscriptions, and routine maintenance as OpEx because these expenses keep your business running month to month. The immediate consumption of these costs means you expense them fully in the period they occur.

Your insurance premiums, office supplies, and professional service fees all fall into this category because they deliver short-term value. You also classify repairs that restore equipment to its original condition (rather than improving it) as operating expenses. This distinction matters because OpEx flows directly to your income statement and reduces your net income in the current period.

Core criteria for CapEx classification

Capital expenditures involve purchasing or improving physical assets that generate value over multiple years. When you buy manufacturing equipment, construct a building, or acquire land, you record these as assets on your balance sheet. The key identifier is longevity paired with substantial cost relative to your normal operating budget.

Asset improvements that extend useful life or enhance productivity also qualify as CapEx. Installing a new HVAC system, upgrading production machinery, or adding capacity to existing facilities all meet the capital expenditure definition. You depreciate these costs across their expected useful life rather than expensing them immediately.

Proper classification of OpEx vs CapEx ensures accurate financial reporting and optimizes your tax deductions across multiple periods.

Accounting and tax impact on financials

Your accounting treatment of OpEx versus CapEx creates vastly different effects on your financial statements and tax obligations. These classification decisions determine when you recognize expenses, how you report asset values, and when you receive tax relief. Understanding these impacts helps you structure purchases strategically and maintain accurate financial records that satisfy auditors and tax authorities.

Financial statement treatment

Operating expenses appear on your income statement as period costs that reduce your net income in the year you incur them. You deduct the full amount from revenue immediately, which lowers your reported profit but also decreases your taxable income for that period. This creates an instant tax benefit while showing higher operational costs on your profit and loss statement.

Capital expenditures follow a different path through your books. You record the initial purchase as an asset on your balance sheet rather than an expense on your income statement. The asset value then transfers gradually to your income statement through depreciation over the asset's useful life. This means a $100,000 equipment purchase might only reduce your net income by $10,000 per year if you depreciate it over 10 years using the straight-line method.

Tax deduction timing and methods

The opex vs capex distinction fundamentally alters when you claim tax deductions. OpEx delivers immediate tax relief because you deduct the entire expense in the current tax year. CapEx spreads your deductions across multiple years through depreciation schedules that match the asset's useful life, whether that's 5 years for computer equipment or 39 years for commercial buildings in many tax jurisdictions.

Tax authorities often provide accelerated depreciation options that let you claim larger deductions in early years. Methods like declining balance depreciation front-load your tax benefits, reducing taxable income faster than straight-line depreciation. Some jurisdictions also offer bonus depreciation or Section 179 expensing that allows immediate deduction of certain capital purchases up to specific limits.

Strategic timing of CapEx purchases and choosing appropriate depreciation methods can significantly optimize your tax position across multiple years.

Your cash flow statement reflects both categories differently as well. OpEx reduces operating cash flow, while CapEx appears in the investing activities section. This separation helps investors and lenders assess how you allocate resources between maintaining operations and building long-term capacity.

Examples and gray areas across industries

You encounter different opex vs capex classifications depending on your industry sector and the nature of your spending. Manufacturing companies typically treat production equipment as CapEx while recording raw materials and labor as OpEx. Software firms classify server infrastructure as capital expenditure but categorize cloud hosting fees as operating expense. Agricultural businesses record land purchases and irrigation systems as CapEx while seed, fertilizer, and seasonal labor fall into OpEx.

Clear-cut examples by industry

Manufacturing operations classify production machinery, factory buildings, and conveyor systems as capital expenditures because these assets produce value for years. Your routine maintenance costs, electricity consumption, and production line staffing all represent operating expenses that support daily output.

Service businesses treat office leases, employee compensation, and marketing campaigns as OpEx since these costs drive current period revenue. Professional equipment like computers or furniture becomes CapEx when you purchase them outright but shifts to OpEx when you lease them under operating lease terms.

Equipment leasing transforms a capital purchase into an operating expense, improving cash flow while maintaining access to essential assets.

Common classification challenges

Software licensing creates significant gray area between OpEx and CapEx categories. You classify perpetual licenses as capital expenditure because you own the software indefinitely, while annual SaaS subscriptions flow through as operating expense. Custom software development for internal use typically qualifies as CapEx when it creates a lasting business asset, but maintenance and updates remain OpEx.

Building improvements present another classification challenge. Major renovations that extend useful life or add functionality qualify as CapEx, while repairs restoring original condition count as OpEx. Installing a new roof represents capital improvement, but patching leaks classifies as operating expense.

Research and development costs vary by jurisdiction and accounting standards. Some frameworks require you to expense R&D immediately as OpEx, while others permit capitalization of certain development costs once technical feasibility is established. Your specific situation determines proper treatment based on applicable accounting standards and tax regulations.

Applying OpEx vs CapEx in capital projects

You face critical classification decisions when evaluating capital projects that determine both immediate cash requirements and long-term financial performance. Every project component requires assessment against the opex vs capex criteria to structure your investment correctly and maximize tax efficiency. Your classification choices affect project approval thresholds, budget allocation, and ultimately the return on investment calculation that determines project viability.

Project evaluation and classification decisions

BioGas processing facilities present typical classification scenarios where you categorize the BioTreater system purchase as CapEx because it represents a physical asset with multi-year utility. Installation costs including site preparation and hookup expenses also qualify as capital expenditure when they enhance the asset's value or extend its useful life beyond original expectations.

Your operating costs for these systems flow through as OpEx, including maintenance contracts, catalyst replacement, electricity consumption, and monitoring software subscriptions. The key distinction lies in whether the expense maintains current functionality (OpEx) or improves capacity and efficiency beyond original specifications (CapEx). Your monthly utility expenses and routine service visits classify as operating expenditure regardless of project size.

Proper classification in project budgets ensures accurate cost-benefit analysis and realistic financial projections for stakeholder approval.

Total cost of ownership considerations

You calculate total project costs by combining initial CapEx outlay with projected OpEx over the asset's useful life. Equipment with lower upfront capital cost but higher operating expenses may deliver worse returns than premium equipment with minimal ongoing costs. Your financial model should incorporate depreciation schedules, tax deduction timing, and maintenance requirements to compare competing solutions accurately. This analysis helps you select equipment that optimizes both categories for maximum profitability across the project lifecycle.

Key takeaways

Your understanding of opex vs capex directly impacts how you structure investments, claim tax deductions, and report financial performance. You classify expenses based on their useful life and benefit duration: operating expenditure covers short-term costs that maintain current operations, while capital expenditure involves purchasing assets that deliver value across multiple years.

Classification decisions affect your cash flow, tax position, and financial statements in fundamentally different ways. OpEx provides immediate tax relief but increases your current period costs, while CapEx builds balance sheet value and spreads deductions over time through depreciation.

When you evaluate equipment purchases or infrastructure investments, apply these principles to optimize your spending strategy. Explore how 99pt5's BioTreater systems deliver superior OpEx efficiency with guaranteed performance metrics that maximize your return on capital investment.